Advertisement

Advertisement

Take Five: Black Friday test

By:

(Reuters) - The most important day for U.S. retailers is here and questions are rife on whether king dollar is set to lose its crown.

(Reuters) – The most important day for U.S. retailers is here and questions are rife on whether king dollar is set to lose its crown.

Global purchasing managers data will shine a light on the health of the world economy, while markets want to see whether Beijing could step up some of its promised support.

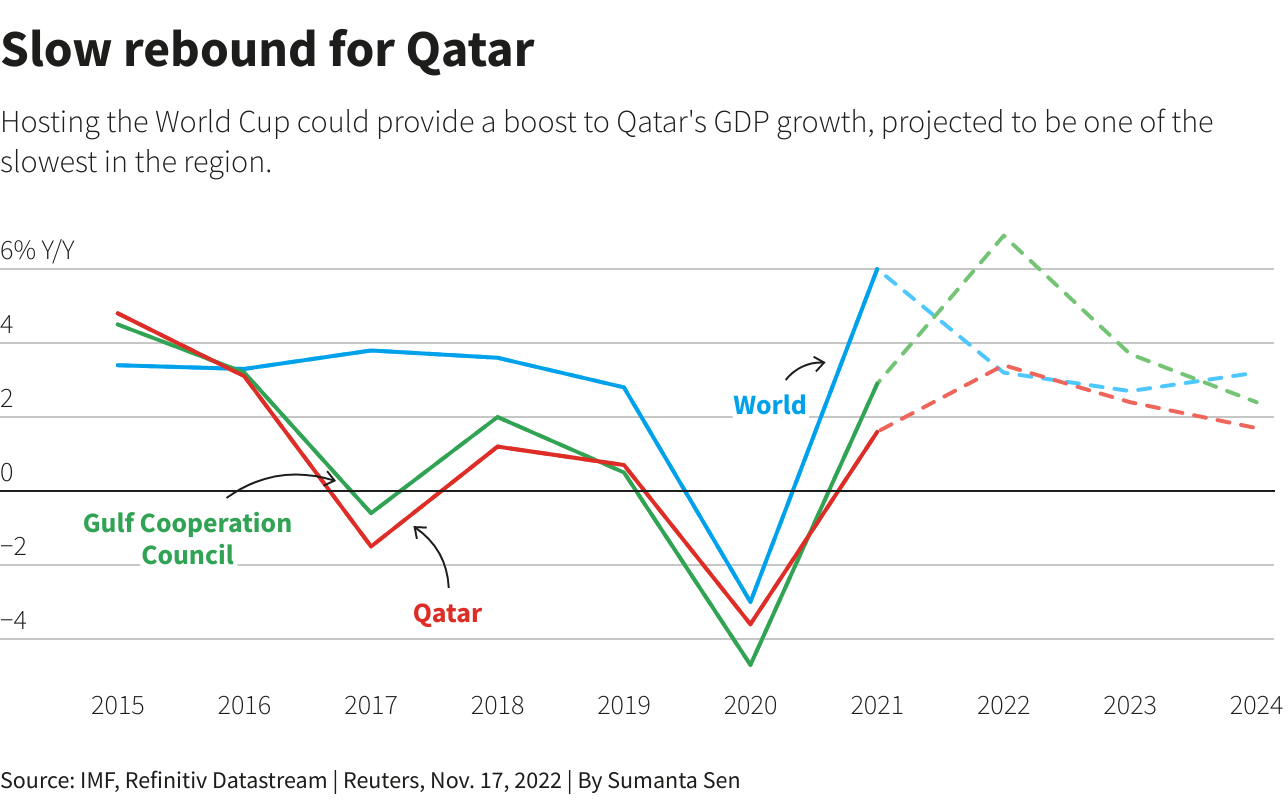

And the World Cup football bonanza is underway in Qatar.

Here’s a look at the week ahead in markets from Lewis Krauskopf in New York, Kevin Buckland in Tokyo and Amanda Cooper, Dara Ranasinghe and Karin Strohecker in London.

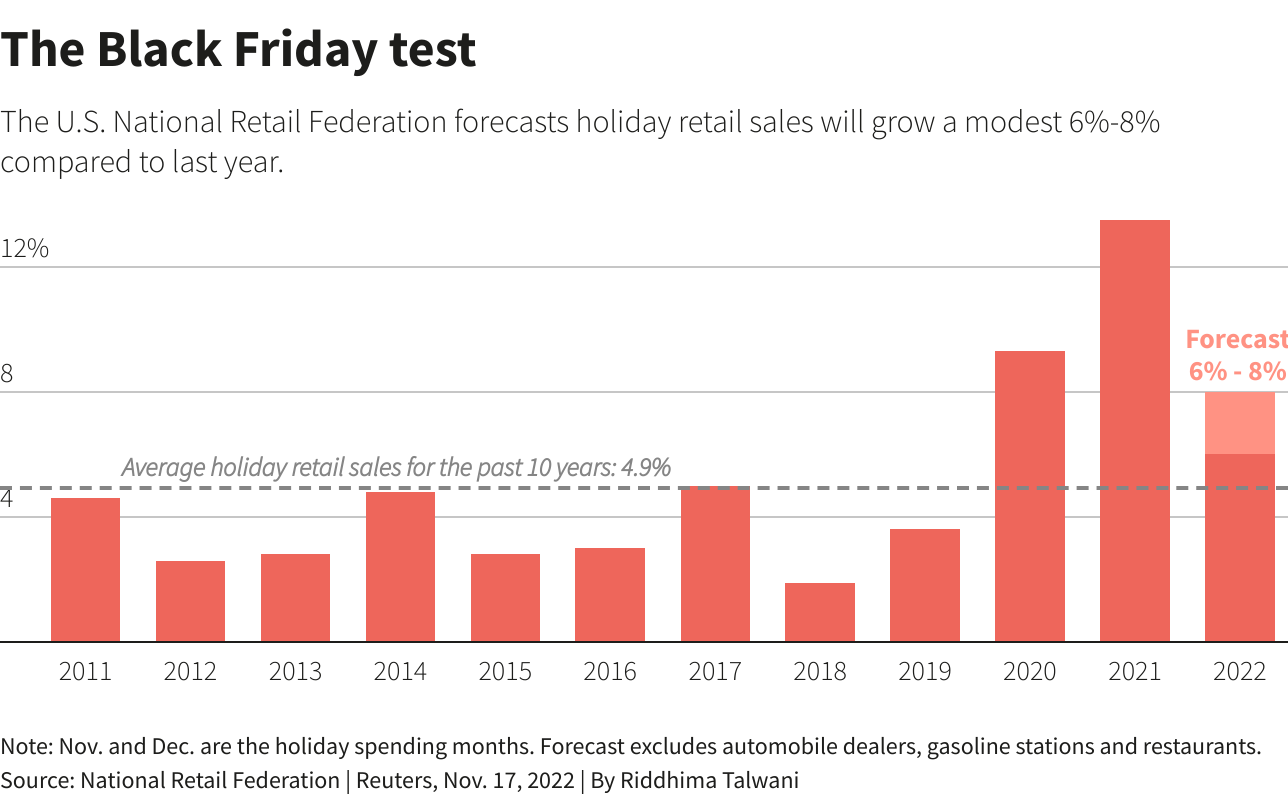

1/GOING SHOPPING With concerns that the U.S. economy may be on the verge of a recession, a key test of consumer demand arrives on Nov. 25, when retailers launch “Black Friday” sales – a day traditionally marked by long lines of shoppers eager to pounce on discounts.

Soaring inflation and surging interest rates could test buying appetite. October U.S. retail sales increased more than expected, boosted by purchases of motor vehicles and a range of other goods, suggesting the consumer may be on more solid footing heading into year-end. Consumer spending accounts for more than two-thirds of U.S. economic activity. Retailers have offered mixed results in the most recent earnings season. Just this week, Walmart lifted its annual sales and profit forecast as demand for groceries was expected to hold up despite higher prices, while Target forecast a surprise drop in holiday-quarter sales.

2/PAST THE PEAK

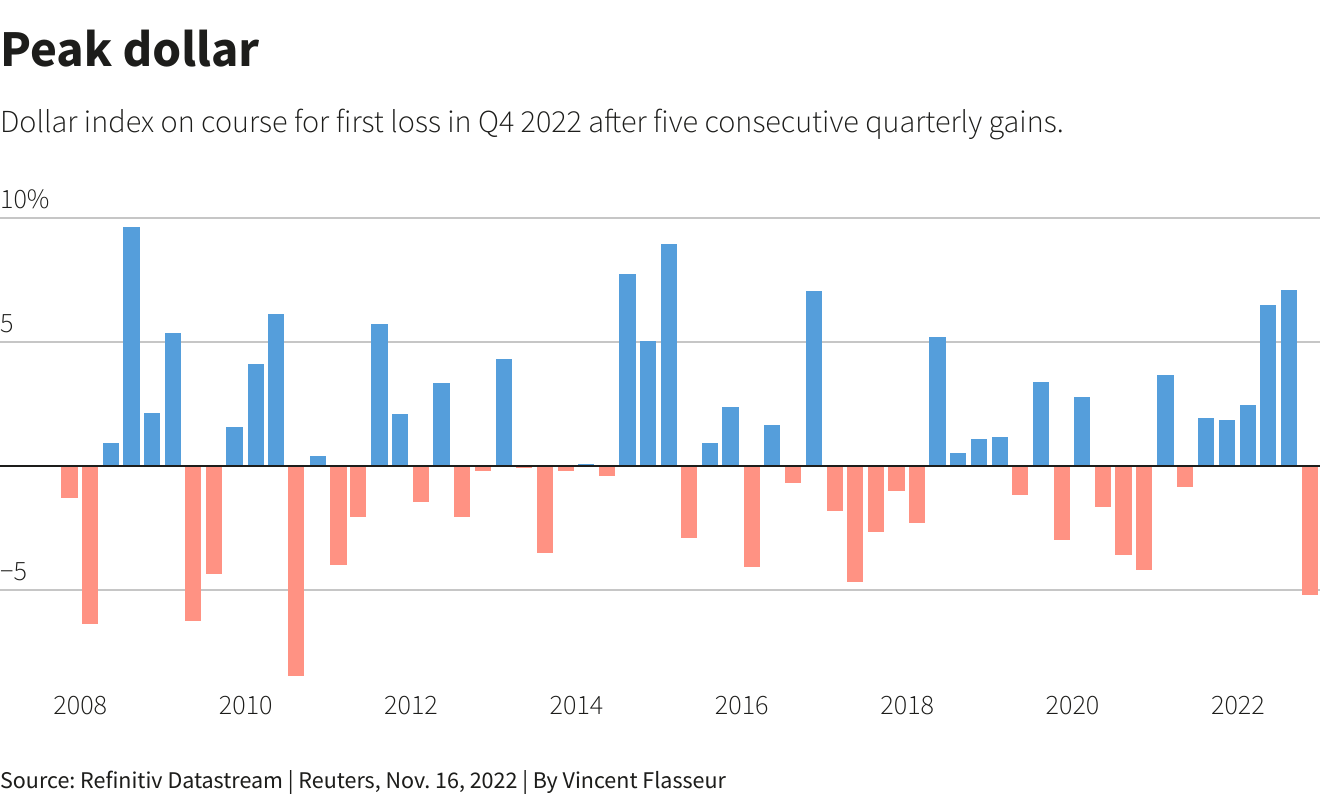

The rise of the U.S. dollar has been the dominant trading theme of 2022, thanks to the Federal Reserve’s quest to raise interest rates to quell inflation, giving the currency an edge over its peers among investors, who have been starved of any kind of yield for at least a decade.

October’s inflation report delivered evidence that consumer price pressures have slowed for the past four straight months from June’s 41-year peak of 9.1%. The dollar index, meanwhile, peaked at a 20-year high of 114.78 in September and has been falling ever since.

Now, it’s heading for its biggest quarterly loss since the second quarter of 2017, having shed 4.5% in value. The time may be fast approaching for dollar bears to emerge from hibernation.

3/BLEAK OUT THERE

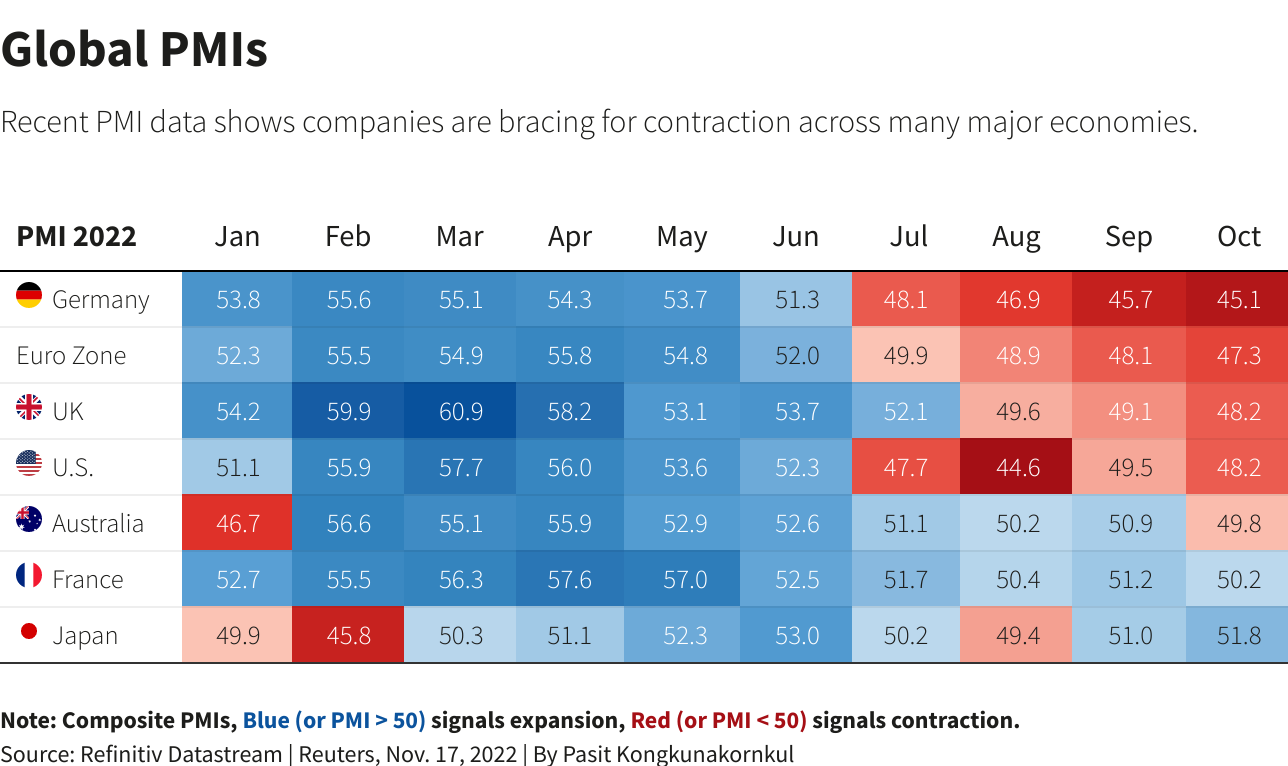

The International Monetary Fund says the global economic outlook is even gloomier than it was a month ago. Is the pessimism justified? Preliminary readings of business activity in November from a number of economies could answer the question in the coming days.

Manufacturing PMIs for October pointed to a deepening contraction in global industry, with developed markets leading the decline. In most European countries, PMIs are below the 50 marker that separates expansion from contraction — France was an exception.

Britain is already facing a lengthy recession. Euro zone economic growth has held up better than expected and labour markets remain relatively robust. But the risk of recession is still elevated for a region grappling with an energy shock and higher costs for anything from financing to wages.

4/ZEROING IN ON CHINA

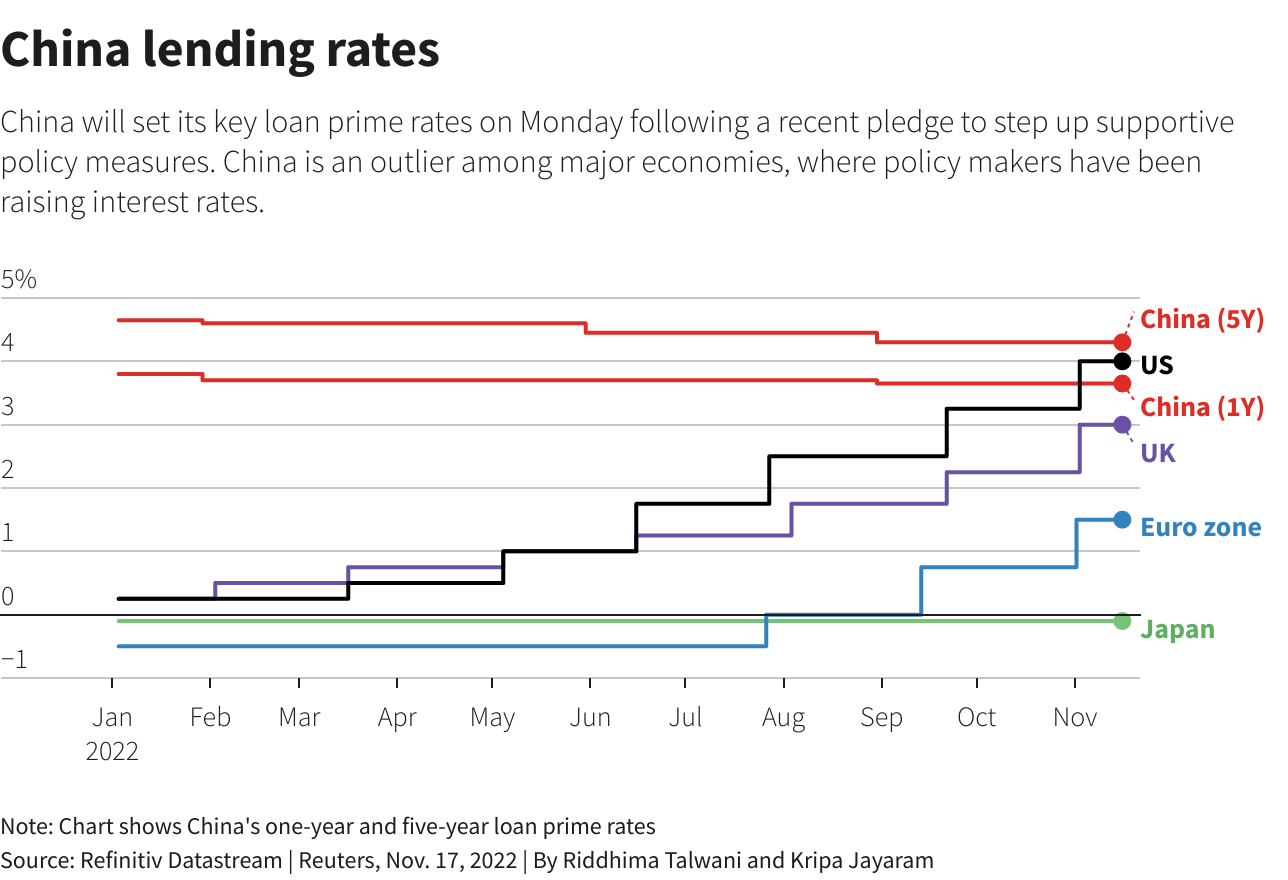

The Chinese central bank’s pledge to step up supportive policy measures are in focus, though policymakers kept benchmark lending rates steady for a third straight month on Monday. Some had expected a cut in the five-year loan prime rate (LPR), though no change suggests the bank remains wary of stoking further yuan weakness by easing monetary conditions.

Stocks and industrial metal markets had cheered signs of pro-growth initiatives, from help for the beleaguered property market to, crucially, an easing of choking zero-COVID policies.

But the COVID outlook remains murky. Noises from Beijing are that “life-saving” measures are essential, which argues against making too much of a two-day reduction in quarantine times. Students in schools across several Beijing districts buckled down for online classes after officials called for residents in some of its hardest-hit areas to stay home.

Other regional central banks will also be setting rates. The Reserve Bank of New Zealand is tipped for a super-sized 75 basis point hike on Wednesday, while the Bank of Korea is seen tightening again, but possibly only by a quarter of a point.

5/ THE BEAUTIFUL GAME

The football World Cup is finally underway – an event marred by controversy since Qatar was awarded hosting rights 12 years ago, including allegations of corruption and human rights violations.

Qatar has much riding on the tournament passing off smoothly – hoping to affirm Doha’s place on the global stage and for an economic boost.

Higher consumption, government spending and services exports are all positives for the Gulf state that has seen its growth outlook trail some of its peers in a region buffeted by high crude prices. But it remains to be seen how long these effects might last, according to analysts.

(Graphics by Sumanta Sen, Riddhima Talwani, Kripa Jayaram, Pasit Kongkunakornul and Vincent Flasseur; Compiled by Karin Strohecker; Editing by Elaine Hardcastle)

About the Author

Reuterscontributor

Reuters, the news and media division of Thomson Reuters, is the world’s largest international multimedia news provider reaching more than one billion people every day. Reuters provides trusted business, financial, national, and international news to professionals via Thomson Reuters desktops, the world's media organizations, and directly to consumers at Reuters.com and via Reuters TV. Learn more about Thomson Reuters products:

Did you find this article useful?

Latest news and analysis

Advertisement