Advertisement

Advertisement

Ten years on, Italy faces debt crisis Draghi may not solve

By:

By Francesco Canepa and Gavin Jones FRANKFURT/ROME (Reuters) - Ten years after his 'whatever it takes' pledge saved the euro, Mario Draghi is once again in the middle of a debt crisis - but the Italian prime minister and former head of the European Central Bank will need more than just words to solve this one.

By Francesco Canepa and Gavin Jones

FRANKFURT/ROME (Reuters) – Ten years after Mario Draghi’s “whatever it takes” pledge saved the euro, Italy is once again in the middle of a debt crisis – but the country’s prime minister and former head of the European Central Bank may struggle to solve this one.

Just like a decade ago, investors are questioning whether some euro zone countries can continue to roll over their public debts, which have ballooned during the pandemic and are becoming more expensive to refinance as the ECB prepares to raise interest rates.

This time, however, the epicentre of the crisis is Italy’s secular lack of economic growth, rather than the financial excesses that landed Greece, Portugal, Ireland and Spain in trouble 10 years ago.

The situation for Italy has just become a lot more unstable.

Draghi offered to resign on Thursday after one of the parties in his fractious coalition refused to back him in a confidence vote, only to have his resignation rejected by the head of state. Draghi is due to address parliament on Wednesday with his future still in the balance.

Italy’s benchmark 10-year yield rose to a high of 3.5% on Thursday and the spread over safer German Bunds widened to 227 points by the close, having more than doubled since the start of the year.

“Things just got worse; how much worse is difficult to tell,” said Dirk Schumacher, an economist at Natixis.

Draghi, 74, dubbed “Super Mario” due to his long career as a financial problem solver, has seen Italian borrowing costs rise during his 17-month premiership, something he acknowledged at a news conference two months ago.

“This shows I’m not a shield against all events. I’m a human being, and so things happen,” he told reporters.

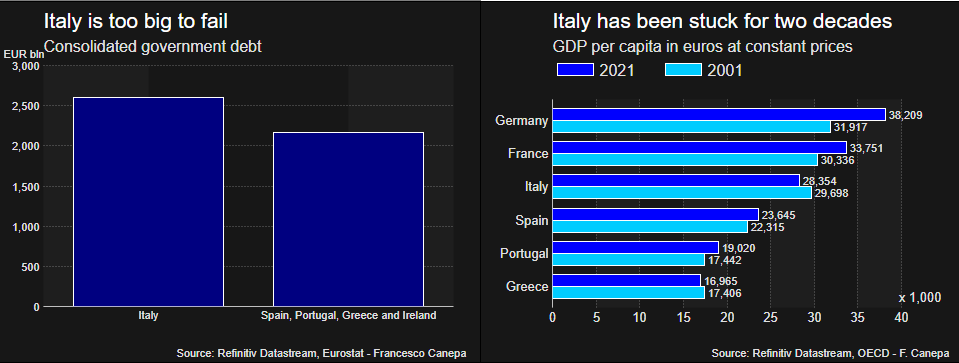

The deeper issue is that Italy is big enough to bring down the rest of the euro zone periphery as its 2.5 trillion euro ($2.52 trillion) government debt pile is larger than those of the other four countries combined and too big for a bailout.

Ten years ago, the then ECB president restored market calm by saying the ECB would do “whatever it takes” to save the euro – code for buying the bonds of troubled countries.

His words on July 26, 2012, reverberate to this day, keeping markets relatively calm on the expectation the ECB will once again put a lid on borrowing costs, including via a new bond-buying scheme now in the works.

But this is only likely to be another stop-gap solution as investors are bound to test the ECB’s resolve for as long as Italy does not convince them it can stand on its own two feet.

“The real problem is that Italy has been a growth underperformer for two decades,” Moritz Kraemer, chief economist at LBBW, said. “And the fiscal situation is not the cause, it’s the consequence of that weakness.”

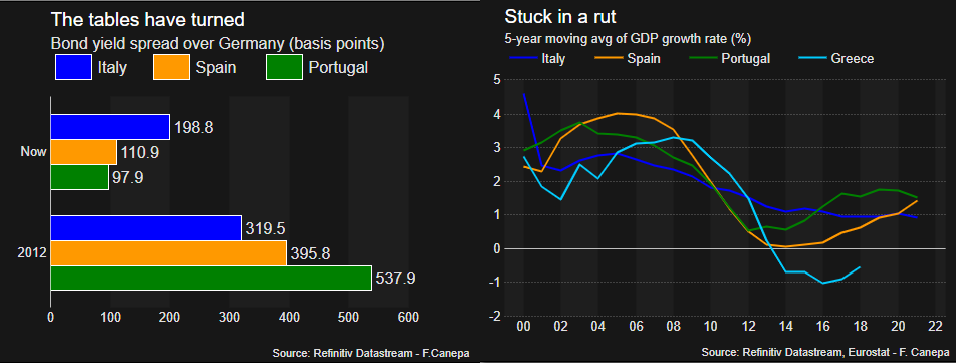

Tables have turned

Italy never had to deal with the bursting of a housing bubble during the global financial crisis and its budget problems were smaller than those of the other four troubled countries.

So it didn’t have to follow them in requesting a bailout from a so called Troika comprised of the International Monetary Fund, the European Commission and the ECB.

It may now come to regret it.

Under pressure and supported by money from international lenders, Portugal fixed its budget, Spain and Ireland cleaned up their banking sectors, and even Greece made reforms including to its pension systems, labour market and product regulations.

Such efforts allowed these countries, to varying degrees, to start growing their economies again.

Italy, by contrast, has not done enough to kick-start growth despite some changes to its pension system, labour market and, under Draghi, its notoriously slow justice system.

As a result, the country that was once seen as the best of a bad lot is now paying the highest premium to borrow on the bond market after Greece – a country that defaulted twice in the past decade and is still rated “junk”.

Lingering anti-euro rhetoric from some right-wing parties is also keeping investors on edge, with Intesa Sanpaolo estimating that the risk of a return of the lira outweighed that of a default in the cost of buying insurance on Italian debt.

“It very much paid off for Spain, Portugal and Greece to have the Troika,” Holger Schmieding, an economist at Berenberg, said.

“Draghi is trying, has done a little bit here and there but neither I nor the market are yet convinced that trend growth in Italy is strong enough.”

Kicked down the road

As ECB chief Draghi regularly stressed the importance of fiscal and other reforms by governments. But as premier of Italy he has had to spend much of his time mediating between parties with very different views on economic policy, meaning contentious issues like tax and pension reforms have been largely kicked down the road.

Even if he rides out Rome’s current political turmoil, with his governing coalition weakened by divisions and general elections looming in the spring of 2023 at the latest, few expect the prime minister to turn things around.

Draghi did finalise a plan presented to the European Union in return for almost 200 billion euros of pandemic recovery funds and ensured a solid start in meeting the hundreds of so-called “targets and milestones” it contains.

But these are mostly small-scale tweaks to legislation – a total of 527 of which will need to be ticked off by 2026, long after Draghi is due to leave office.

This money, made up of grants and cheap loans, could prove a lifeline for Italy if it needs to tighten its own budget.

But the country’s track record on using financial help from Brussels is dismal. It managed to spend only half its EU funds in the last budget cycle, the second lowest share after Spain.

LOST DECADE(S)

In fairness to Draghi and his predecessors, Italy’s malaise is much older than the global financial crisis.

Its GDP per capita is lower now than 20 years ago, when it was only a touch below France’s and Germany’s.

All other European countries have grown over that period except Greece which has shrunk by less, leaving Italy as the worst performer in the bloc.

Trend growth – or the average rate of increase over the economic cycle – is pointing up across all the so-called peripheral countries except for Italy, Eurostat data shows.

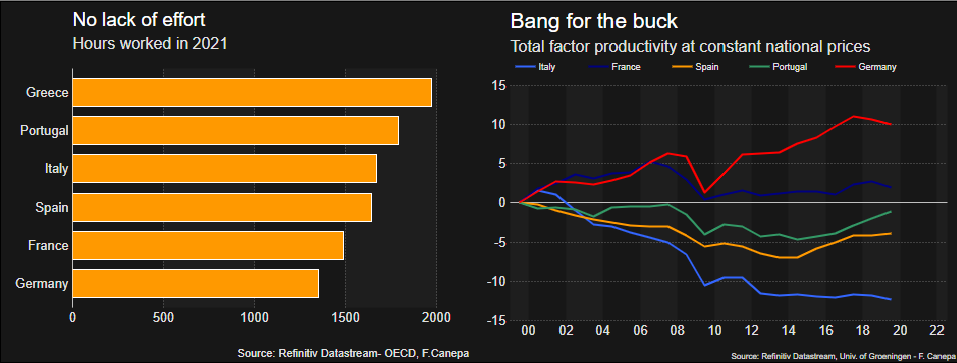

Italian productivity – or how much economic output is squeezed out of an hour worked or a euro invested – stopped growing in the 1990s and has since fallen.

Behind this lies a web of problems that include a rapidly ageing population, a low-skilled workforce, cloying red tape, a slow and dysfunctional justice system and chronic under-investment in education, infrastructure and new technology.

Many euro zone countries have some of these problems, but few if any have all of them.

Some economists including Chicago Booth School of Business professor Luigi Zingales say Italy essentially missed the digital revolution and blame what they call the Italian disease of entrepreneurs who opt to keep a small business in the family rather than grow it with the help of outside investors.

By joining the euro, Italy also lost the quick fix of being able to devalue its currency – a trick that helped Italian industry prosper for decades by making its exports cheap.

“We chose the wrong growth model back in the 1980s,” said Francesco Saraceno, economics professor at Rome’s Luiss University and Sciences-Po in Paris.

“To respond to globalisation we tried to compete with emerging markets by lowering costs instead of following the German example of investing in higher-quality production.”

($1 = 0.9917 euros)

(Reporting by Francesco Canepa and Gavin Jones; Additional reporting by Giuseppe Fonte and Dhara Ranasinghe; Editing by Susan Fenton and Daniel Wallis)

About the Author

Reuterscontributor

Reuters, the news and media division of Thomson Reuters, is the world’s largest international multimedia news provider reaching more than one billion people every day. Reuters provides trusted business, financial, national, and international news to professionals via Thomson Reuters desktops, the world's media organizations, and directly to consumers at Reuters.com and via Reuters TV. Learn more about Thomson Reuters products:

Advertisement