Advertisement

Advertisement

Sleepy FX Markets are a Sign of Complacency, Investors Warn

By:

LONDON (Reuters) - Hedging costs for foreign exchange swings across the world's 10 most-traded currencies have dropped in recent weeks, causing market watchers to warn of investor complacency and to encourage the buying of protection against future volatility.

By Ritvik Carvalho

Implied volatility – which measures the cost of buying options to protect against FX moves – across the ‘G10’ group of currencies has fallen on aggregate in recent weeks, implying that traders expect currencies to be calm in the months ahead.

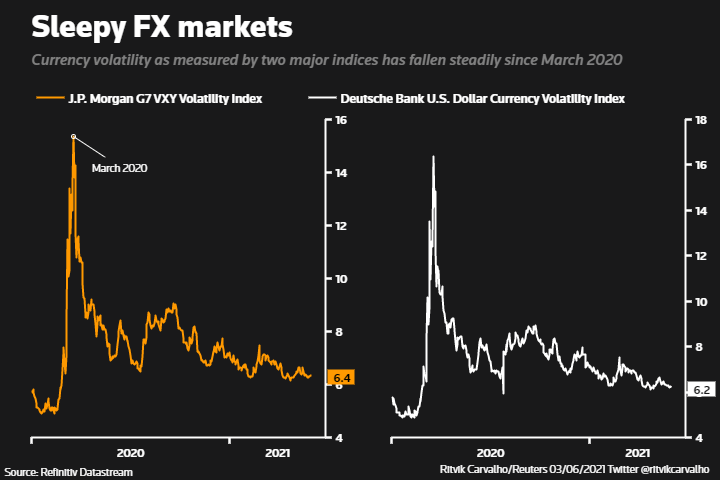

Deutsche Bank’s currency volatility index, which shows an average of 3-month implied volatility for the major currency pairs has fallen to its lowest since July 2020.

Meanwhile, JP Morgan’s G7 currency volatility index has hit lows not seen since March 2020, when a selloff in global markets drove a dash for dollars.

The drop in these gauges reflects a broader phenomenon across financial markets – the suppression of volatility by central banks that have eased monetary policy to unprecedented levels to cushion against the economic devastation wrought by the pandemic.

However, as vaccine rollouts allow economies to reopen and inflation expectations rise, some central banks, including the Bank of Canada and the Bank of England, have begun to taper asset purchase programmes. Others such as the U.S. Federal Reserve have hinted there will be an end to such easy money, even if not yet.

Typically, shifts in central bank policy spark increased volatility in currencies as investors price in diverging monetary policies between countries.

“Should we see some surprises in the evolution of interest rates, these are likely to also affect exchange rates – especially if the rate movements are asynchronous between jurisdictions,” Kambiz Kazemi, CIO at Validus Risk Management, said.

Some investors advise capitalising on the current low cost of options – which they call an indicator of market complacency – as an opportunity to buy protection against future swings.

“It is concerning because when we see aggregate G10 vols below 6%, it’s typically been seen as a good level to get long volatility,” said Peter Kinsella, head of FX strategy at Swiss private bank UBP, citing the 1-month tenor on the J.P. Morgan G7 volatility index.

“To my mind it does show that markets are somewhat complacent.”

Another indicator of low volatility is tight currency trading ranges. The spread between the annual high and low of the euro/dollar pair so far in 2021 is just above 6 cents, and – five months into the year – the narrowest of any year in the single currency’s history.

(Graphic- 2021: narrowest trading range in the euro’s history – https://fingfx.thomsonreuters.com/gfx/mkt/qmyvmzkjepr/Pasted%20image%201622713925456.png)

“In our view, the dichotomy between this multi-decade ‘calm’ currency price action and the fundamentals (rates, inflation expectations, commodity and equity price action) is likely to result in more volatility and changing prices in the medium to long-term,” Kazemi said.

(Reporting by Ritvik Carvalho; editing by Barbara Lewis)

About the Author

Reuterscontributor

Reuters, the news and media division of Thomson Reuters, is the world’s largest international multimedia news provider reaching more than one billion people every day. Reuters provides trusted business, financial, national, and international news to professionals via Thomson Reuters desktops, the world's media organizations, and directly to consumers at Reuters.com and via Reuters TV. Learn more about Thomson Reuters products:

Advertisement