Advertisement

Advertisement

Marketmind: Are we calling it a banking crisis, shock … or blip?

By:

By Jamie McGeever (Reuters) - A look at the day ahead in Asian markets from Jamie McGeever.

By Jamie McGeever

(Reuters) – A look at the day ahead in Asian markets from Jamie McGeever.

Top-tier Chinese economic data including first-quarter GDP grabs the Asian spotlight this week, as investors across the region and beyond weigh whether the U.S. banking ‘crisis’ is in the rear view mirror or if there’s more serious trouble ahead.

The Asian calendar on Monday is light, with only Indonesian trade and Indian wholesale price inflation potentially moving markets. Indonesia’s central bank begins a two-day meeting, and will announce its policy decision on Tuesday.

Investors will also have the first opportunity to react to two developments over the weekend – a policy steer from China’s central bank chief, and Saturday’s apparent attack on Japanese Prime Minister Fumio Kishida.

People’s Bank of China Governor Yi Gang said China can phase out currency intervention by gradually reducing the amount and frequency of its forays into the market, underscoring Beijing’s resolve to boost the yuan’s global presence.

Yi also said the central bank will seek to get real interest rates slightly below the potential growth rate.

Meanwhile, in Japan on Saturday, bodyguards bundled PM Kishida to safety after a man threw what appeared to be a smoke bomb at him during an election campaign stop at a fishing port in the west of the country. This was an eerie reminder of the assassination of former PM Shinzo Abe last year.

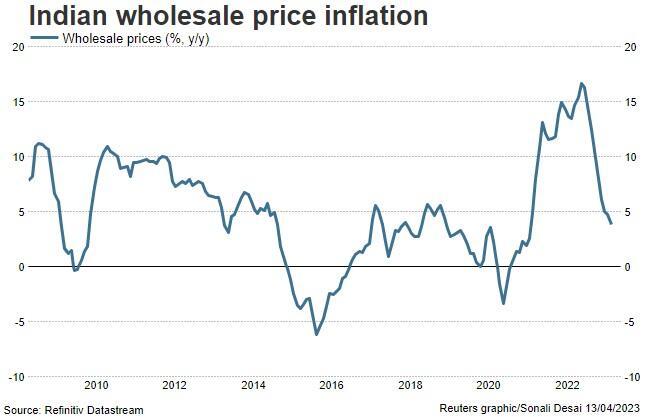

Figures on Monday are expected to show that wholesale price inflation in India virtually halved in March to a 1.87% annual rate from 3.85%. It was 16% less than a year ago.

Investors expect data on Tuesday to show that China’s gross domestic product growth rose sharply in the first quarter after COVID-19 lockdown restrictions were lifted, up 4.0% from a year ago and up 2.9% in the previous three months.

Don’t be surprised by an upside event – China’s economic surprises index is at its highest in 17 years.

The broader tone this week will be set by investors’ stance on the U.S. banking crisis. Or shock. Or blip. The solid recovery in equities and slump in market volatility gauges suggests investors are increasingly sanguine.

Some big U.S. banks on Friday reported strong Q1 earnings – JP Morgan shares surged 7.5% – fueling hopes that the policymakers’ bold and swift action a month ago has worked.

The S&P 500 and MSCI World Index have rebounded almost 10% from the March low, while euro zone stocks on Friday hit their highest level in 22 years.

But complacency would be dangerous. As Morgan Stanley analysts note, U.S. credit growth is shrinking, credit availability for small businesses fell in March at its fastest rate in 20 years, and interest costs are at a 15-year high.

Here are three key developments that could provide more direction to markets on Monday:

– G7 foreign ministers summit in Japan

– India WPI inflation (March)

– ECB’s Christine Lagarde speaks in New York

(By Jamie McGeever; Editing by Diane Craft)

About the Author

Reuterscontributor

Reuters, the news and media division of Thomson Reuters, is the world’s largest international multimedia news provider reaching more than one billion people every day. Reuters provides trusted business, financial, national, and international news to professionals via Thomson Reuters desktops, the world's media organizations, and directly to consumers at Reuters.com and via Reuters TV. Learn more about Thomson Reuters products:

Advertisement