Advertisement

Advertisement

Marketmind: Oil prices fuel the tightening dilemma further

By:

A look at the day ahead in markets from Julien Ponthus.

A look at the day ahead in markets from Julien Ponthus.

There’s arguably little central banks can do to tame surging energy and commodity prices other than try to limit second-round effects as they are being absorbed by the economy.

With oil prices jumping over $3 this morning and Brent above $110 a barrel, investors will be keen to hear later on today from Federal Reserve Chair Jerome Powell and European Central Bank President Christine Lagarde how monetary policy can adjust without rocking the boat of the recovery.

Strategists are indeed keeping a close eye on the spread between yields between of U.S. two-year and 10-year notes, fearing an inversion of that part of the curve could signal an impending recession.

In Germany, producers prices (PPI) show another 1.4% rise on the month, though slightly less than expected, giving another update about how the euro zone’s biggest economy is coping after investor sentiment suffered a record slide in March with collapsing expectations making a recession, a scenario that can no longer be totally dismissed.

Fuelling the latest spike in crude prices is the European Union governments considering whether to impose an oil embargo on Russia over its invasion of Ukraine.

Such a decision, even with public opinion overwhelmingly on the side of Ukraine, could cost EU leaders dearly politically.

Euro zone consumers are getting a taste of what two euros per litre of gasoline tastes and France’s Emmanuel Macron, seeking reelection next month, knows only too well that the “yellow vest” street rebellion was born out of a backlash against higher fuel prices.

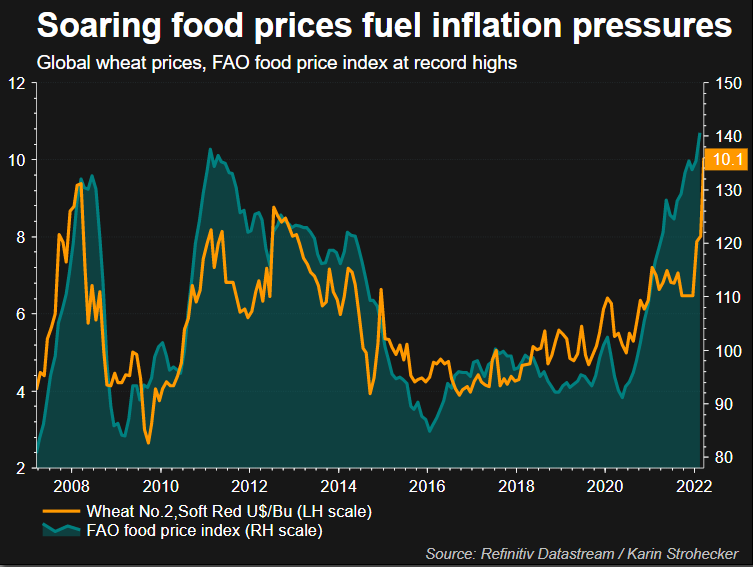

Wheat prices also are at levels seen during the 2007/2008 food crisis, widely regarded as a key factor in the Arab Spring uprisings in the Middle East.

So far, the early monetary tightening cycle has been well received and the Fed’s first hike saw U.S. and European stock markets experience their best week since November 2020, when the COVID-19 vaccine breakthrough lifted global markets.

European futures are broadly flat ahead of cash trading this morning after MSCI’s broadest index of Asia-Pacific shares outside Japan eased 0.7%.

With markets already on hedge, traders will be keen to discover why shares of embattled property developer China Evergrande Group have been suspended pending an announcement by the company.

Meanwhile investors in Russia will closely watch domestic sovereign bonds resuming trading today after a month-long suspension in the wake of Moscow’s invasion of Ukraine.

Key developments that should provide more direction to markets on Monday:

-Russia allows some more financial market operations over next two weeks

-China keeps benchmark lending rates unchanged, as expected [nAZN02ALI3)

-Asking prices for UK houses see biggest March rise since 2004

-Speech by ECB President Christine Lagarde

-Fed speakers: Chairman Jerome Powell, Atlanta Fed President Raphael Bostic

(Reporting by Julien Ponthus)

About the Author

Reuterscontributor

Reuters, the news and media division of Thomson Reuters, is the world’s largest international multimedia news provider reaching more than one billion people every day. Reuters provides trusted business, financial, national, and international news to professionals via Thomson Reuters desktops, the world's media organizations, and directly to consumers at Reuters.com and via Reuters TV. Learn more about Thomson Reuters products:

Advertisement