Retail traders have access to several protections designed to shield them from sudden market swings, broker failures, and other unexpected risks. Understanding how these safety nets work and how to maximize them is key to building long-term trading success.

However, these protections are only as strong as the rules behind them. That’s why it’s so important to choose a broker that’s licensed and strictly regulated by a trusted financial authority.

Indirect trading risks, or counterparty risks,’ arise from the broker’s operations, including how the broker manages client money and corporate capital.

Below, I covered safety measures against indirect trading risks.

All financial regulators, from Tier-1 to offshore, mandate brokers to keep their clients’ funds in separate (segregated) bank accounts from the ones used for their capital.

The purpose is twofold. Firstly, it effectively minimizes the risk of accounting errors (mixing client funds with corporate capital) and other malpractices. Secondly, even if the company becomes insolvent, its clients’ funds will remain protected and uninvolved in the bankruptcy process.

To verify compliance with this requirement, regulators mandate periodic audits (both internal and external) of the broker’s accounts.

Some financial regulators, particularly in Europe (CySEC, BaFin, etc.), require licensed brokers to participate in a compensation scheme. This ensures that even if brokers default on their credit risk, their clients will be reimbursed for their losses.

All brokers participating in a compensation scheme are required to deposit a specified amount of money into a common pool (collateral), which essentially finances the scheme. In the unlikely event that one of the participants becomes insolvent, this common pool can cover its liabilities.

Here is a list of the most popular compensation schemes according to region:

| Country | Compensation Scheme | Compensation Amount |

| Switzerland | esisuisse | Up to CHF 100,000 |

| UK | Financial Services Compensation Scheme (FSCS) | Up to GBP 85,000 |

| Hong Kong | Investor Compensation Fund (ICF) | Up to HKD 500,000 |

| Luxembourg | ICS | Up to EUR 25,000 |

| EEA | Investor Compensation Fund (ICF) | Up to EUR 20,000 |

Some brokers who want to go above and beyond regarding client protection issue private indemnity insurance, which essentially replaces compensation schemes.

Where a broker entity is not required by its regulator to participate in a compensation scheme (or may want to provide an additional layer of protection), the subsidiary may issue such private insurance.

The only difference is that the underwriter of the insurance is a private company (e.g., Lloyd’s London). Individuals protected under private indemnity insurance might be liable for a protection of up to $1,000,000.

In cases where a broker entity participates in a compensation scheme and has also issued private indemnity insurance, its clients can request compensation from both.

Direct trading risk refers to any activity by the trader that endangers their account balance.

When it comes to direct trading risk, traders are provided with three layers of protection by their brokers:

To understand why they are needed and how they function, it is first important to understand the impact of leverage and the risks that come with it.

When you trade Forex and CFD products with a broker, you are essentially trading on margin, whereby the broker lends you the funds to open much larger positions thanks to the so-called leverage. The leverage multiplies a trader’s profits from winning positions and losses from failed trades.

The table below shows how much available margin (funds to trade with) you would have with the same $100 at different leverage rates:

| Used Margin | Leverage | Available Margin |

| $100 | 1:1 | $100 |

| $100 | 1:10 | $1000 |

| $100 | 1:30 | $3000 |

| $100 | 1:50 | $5000 |

| $100 | 1:100 | $10,000 |

Hence, a 1:50 leverage would multiply the profits from winning trades by 50 times, and similarly, it would also amplify losses from losing trades by the same factor.

That’s why many top-tier regulators cap the maximum allowed retail leverage, usually at 1:30 (ESMA, FCA, ASIC, and others). This limit is necessary to prevent inexperienced retail traders from draining their accounts with one or two misguided trades.

On the other hand, many brokers regulated offshore are not required to impose such restrictions, and the maximum leverage with some offshore brokers can reach as high as 1:3000.

Due to leverage’s ambiguity, brokers implement a margin call policy. This serves as a trader’s second line of defense against market unpredictability, with tight stop-loss orders being the first.

Read our dedicated article on leverage and margin to better understand this topic.

Brokers issue margin calls to notify their clients when the risk to their account balance reaches a critical threshold. Essentially, a margin call is an alert that prompts the trader to either deposit additional funds to meet the margin requirements or start closing open trades if running losses exceed this threshold.

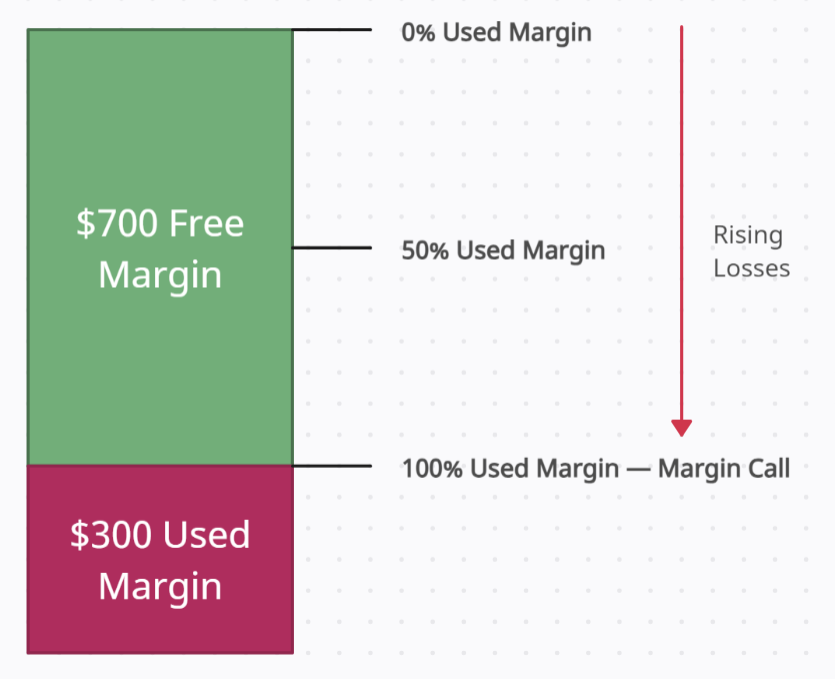

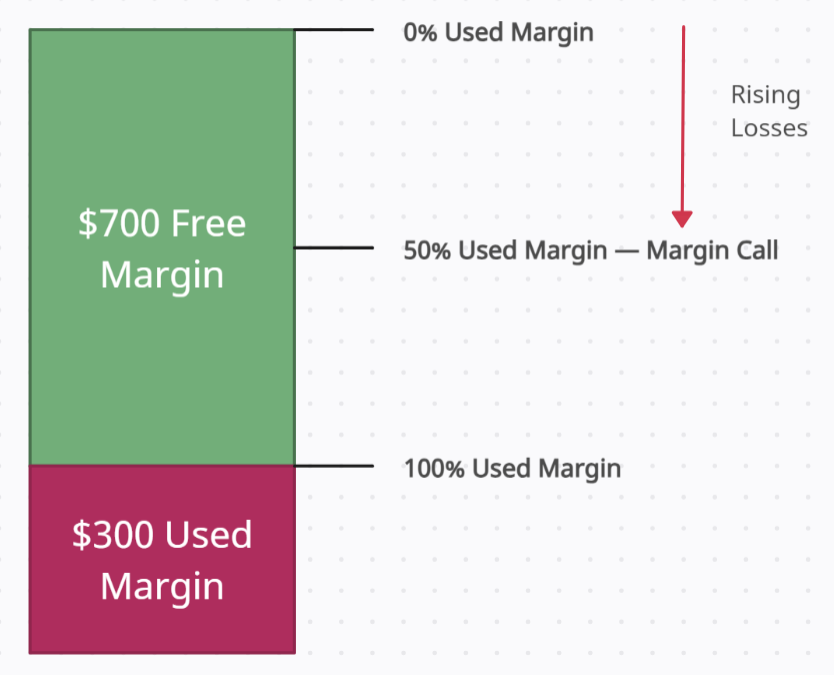

To understand the role of margin calls in real trading, consider the following two scenarios. In the first case, the margin call is set at 100%, and in the second, it is at 50%.

You deposit $1000 in your trading account and use $300 to open a trade. Immediately after your trade is opened, you still haven’t generated profits or incurred losses. You have used $300 of your account balance and have $700 remaining as a free margin.

Since the margin call is set at 100%, you would only receive such a notification if your running losses reach $700. In other words, a margin call occurs when your account’s free margin is used up, yet you still have open trades.

The account balance is $1,000, with $300 used to open a position. Like in the previous scenario, the initial free margin is $700. However, in this case, since the margin call is set at 50% of the free margin, a margin call notification will be issued if the running loss reaches $350.

It follows that brokers with tighter margin call policies are generally safer. That is, their clients would receive margin calls sooner rather than later and can, therefore, react to mounting losses faster.

Pro Tip: If you are an inexperienced trader, it is better to choose a broker with a tighter margin call threshold (below 100%).

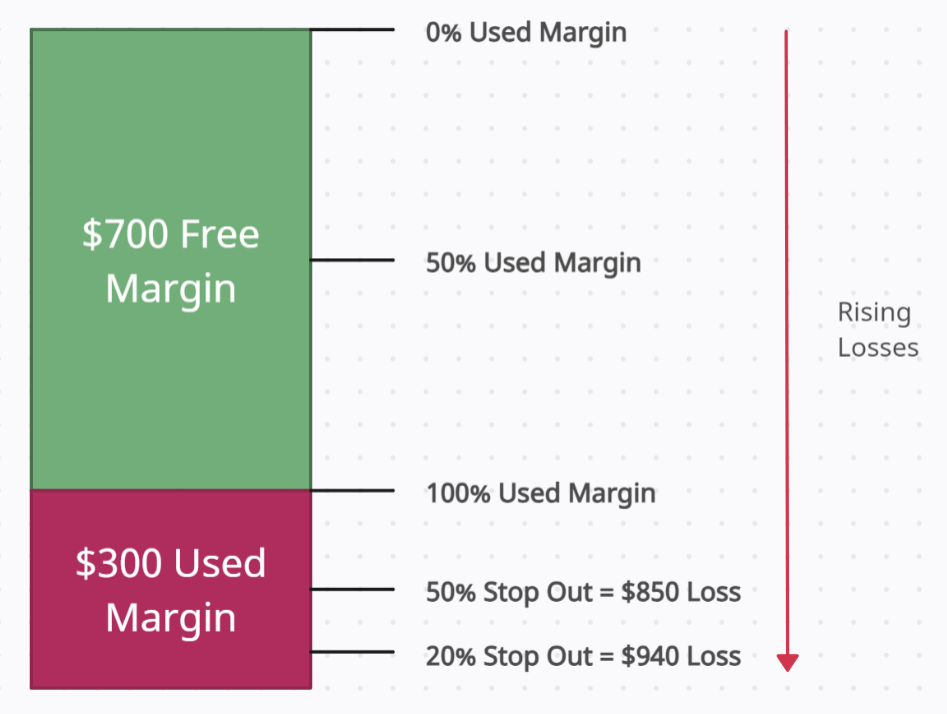

If the margin call level represents the threshold at which your broker sends out a warning and urges you to free up some margin (by closing your losing positions or depositing additional funds), the stop-out level is the next threshold at which the broker begins to close your losing trades, either partially or fully automatically.

In other words, if your margin level drops to the stop-out level, your positions will begin to be liquidated. Thus, the stop-out is your last line of defense before potentially losing your entire account equity.

Once the margin call level is reached, the stop-out is calculated with respect to the remaining used margin. Returning to the examples above, if the stop-out level is set at 50%, this would equate to a net loss of $850 after the stop-out is triggered. This calculation arises because 50% of the $300 used margin is $150, which is added to the running loss of $700. Similarly, if the stop-out is set at 20%, this would result in a net loss of $960.

It follows that brokers with higher stop-out thresholds are generally safer because running losses are liquidated sooner rather than later.

Negative balance protection is arguably the most important safety mechanism. It removes the possibility of a trader’s losses from exceeding his or her account balance. Essentially, it means that you cannot lose more than what you have deposited in your account. But why should it even be necessary to have negative balance protection if there is a stop-out level in place?

In the most extreme example from above, the stop-out level was set at 20%, which equates to a loss of $940. In an ideal scenario, the losing trade would be terminated instantly, and you would be left with an account equity of $60.

But suppose that the stop-out level is reached during heightened market volatility, such as during a press release or a major economic release. This causes the market to move even faster, outpacing the speed of the liquidation process. So, you incur an additional loss of $70, which would result in negative equity. In other words, you would owe your broker $10 because of your poor risk management and its slow order liquidation process.

This is where negative balance protection comes into play. It essentially shifts the credit liability from the trader to the broker, who is now responsible for covering the difference (in this case, the $10). The end result is that the trader is left with no equity in the account ($0 account balance).

Multiple safety mechanisms are in place to protect retail traders from direct and indirect trading risks. A trader’s first job is to find a tightly regulated broker to ensure that these are indeed available.

Some of the most important safety mechanisms against indirect trading risks include the segregation of client funds and the availability of compensation schemes or private insurance. With respect to direct trading risks, retail traders are protected on several tiers: using margin calls, stop-out levels, and, in extreme cases, negative balance protection.

Finance writer, analyst, and author of a book for beginner traders "Bulls, Bears and Sharks" with an experience of over 8 years in retail trading and more than 3 years in the finance area.