Advertisement

Advertisement

Analysis-Investors warm to European corporate bonds after a brutal year

By:

By Harry Robertson LONDON (Reuters) - Investors are moving back into the European corporate bond market after one of the most brutal years in history, lured by juicy yields and hopes that central banks may soon let up on their aggressive interest rate hikes.

By Harry Robertson

LONDON (Reuters) – Investors are moving back into the European corporate bond market after one of the most brutal years in history, lured by juicy yields and hopes that central banks may soon let up on their aggressive interest rate hikes.

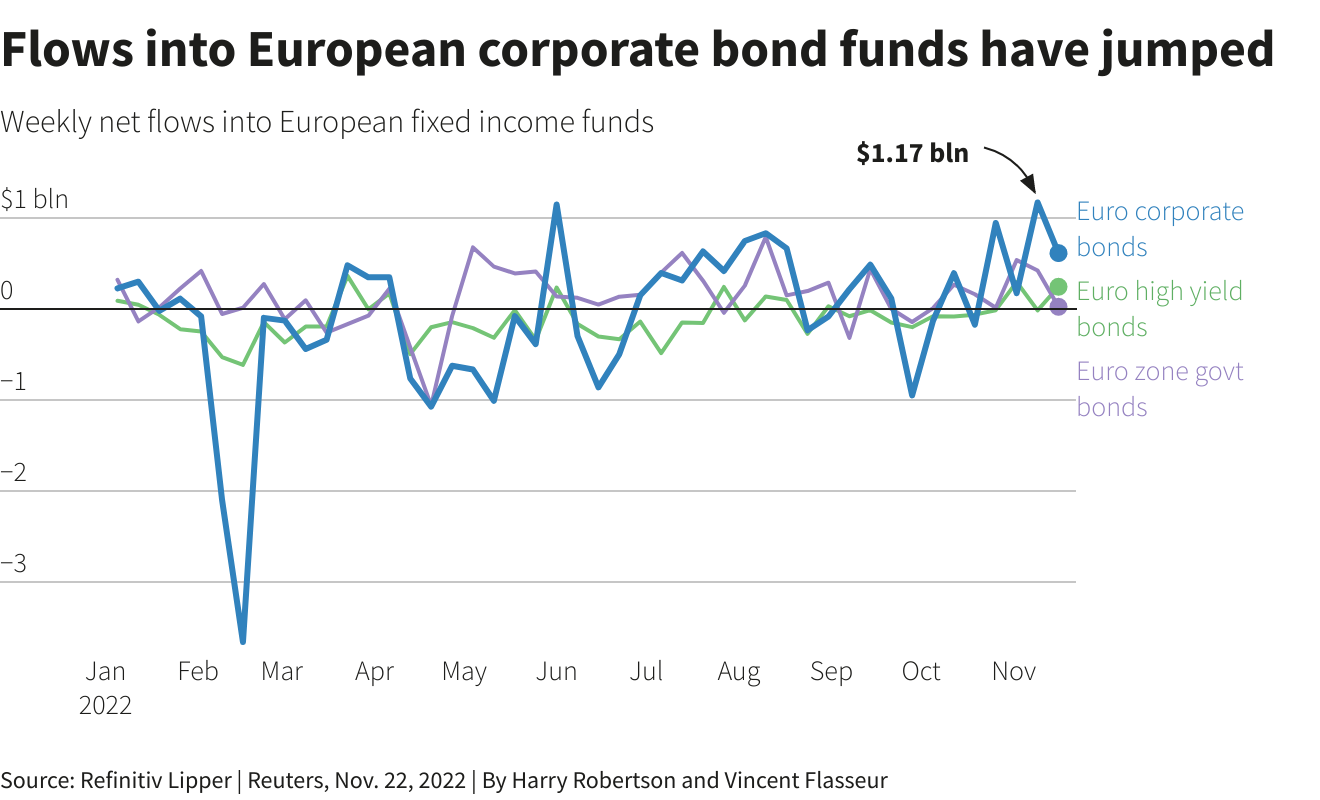

Funds focused on investment grade euro-denominated corporate debt have seen sizeable inflows for four straight weeks, according to data from Refinitiv Lipper, even as Europe teeters on the brink of recession.

Net inflows came in at $1.17 billion in the week to Nov. 9, the highest weekly amount this year.

Data from BlackRock tells a similar story. A net $3.62 billion flowed into BlackRock’s exchange-traded products which track investment grade European corporate debt in the 30 days to November 17. The asset manager said it was a marked pick-up which outstripped flows into government bonds.

“We are at the beginning of a rotation as investors come back into credit,” said Carolyn Weinberg, global head of product for ETF and index investments at BlackRock. “Our clients are buying government bonds and investment grade bonds.”

Underpinning the renewed interest are investors’ bets that the pain from central bank rate hikes is almost over.

With latest data showing U.S. inflation cooling, traders now expect fewer rate hikes from the Federal Reserve, which lifts some of the pressure off the European Central Bank. This has buoyed government bond prices, pushing their yields down, and boosted riskier assets such as corporate bonds and stocks.

The iBoxx euro corporate bond index has risen almost 4% since hitting an eight-year low in October, although it remains down 13% for the year.

Higher yields attract investors

After a dramatic sell-off in both bonds and equities in 2022, and inflation easing from sky-high levels, the stage is set for a rebound in both assets, according to Denise Chisholm, director of quantitative markets strategy at Fidelity Investments.

“We can see a situation where both stocks and bonds are actually positive from a total return perspective over the next six months,” she said.

Higher yields are a big draw. Bond yields, which move inversely to prices, shot upwards as fixed income markets crashed this year. Now investors can get yields of around 4% or more on short-dated bonds issued by companies with strong credit ratings, up from less than 1% at the start of the year.

The dividend yield on the STOXX 600 for example is lower at 3.37%, according to Refinitiv data.

“For the first time in a very long time you can get a decent real return for buying not just government bonds, but also the higher quality parts of the bond market,” said Seamus Mac Gorain, head of the global rates team at JPMorgan Asset Management.

Goldman Sachs strategists recently told clients that one- to five-year European corporate bonds are “very attractive”. They said they’re more appealingly priced than U.S. corporate debt, with many investors overly pessimistic about the outlook for Europe’s economy.

Uncertainty remains

A warm October has lifted the pressure on the continent’s energy system and sent natural gas prices tumbling, a move that’s likely to be welcomed by ECB policymakers grappling with inflation and governments scrambling to help households and businesses cope with high energy bills.

“If you have a sharp fall in energy prices and gas prices at the margin, that’s useful for corporate earnings,” said Mike Riddell, a senior portfolio manager at Allianz Global Investors.

Yet for Riddell, government debt looks like a better bet than corporate bonds. He said Europe is heading for a bleaker recession than many investors expect and uncertainty is high.

“Even though gas prices have fallen very sharply, there are clearly major risks of yet more supply shocks and yet more increases in inflation,” he said.

Economic uncertainty means JPMorgan’s Mac Gorain is steering clear of high-yield debt, issued by companies with weaker credit ratings.

“We’re still a bit more wary of the lower quality parts of the credit markets, just because we do think that recession is still the base case for next year,” he said.

(Reporting by Harry Robertson; Editing by Emelia Sithole-Matarise)

About the Author

Reuterscontributor

Reuters, the news and media division of Thomson Reuters, is the world’s largest international multimedia news provider reaching more than one billion people every day. Reuters provides trusted business, financial, national, and international news to professionals via Thomson Reuters desktops, the world's media organizations, and directly to consumers at Reuters.com and via Reuters TV. Learn more about Thomson Reuters products:

Did you find this article useful?

Latest news and analysis

Advertisement