Advertisement

Advertisement

Marketmind: Too flashy?

By:

A look at the day ahead in U.S. and global markets from Mike Dolan.

A look at the day ahead in U.S. and global markets from Mike Dolan.

If investors’ big concern about the new year is that the U.S. economy is running too hot, then February’s flash business surveys from around the world will do little to soothe nerves.

U.S. markets return from Monday’s Presidents Day holiday and the early readout on this month’s factory and service sector activity tops the slate. European equivalents out already on Tuesday are showing a sharp pickup, with services leading the private sector back into a brisk expansion that’s far above forecasts.

Even the mood in gloomy Britain brightened.

While an easing of Europe’s energy shock during the mild winter has been a significant regional factor, the boost to confidence tallies with booming U.S. labour markets and retail sales for January and the re-emergence of China from its COVID lockdowns.

The debate is no longer about whether there’s a hard or soft landing for the world economy this year, it’s whether there is any landing at all.

The problem for markets is that dodging a recession and re-acceleration of global growth also makes it more difficult to get sticky inflation rates back to central bank targets and pushes any hope of interest rate easing this year off the agenda.

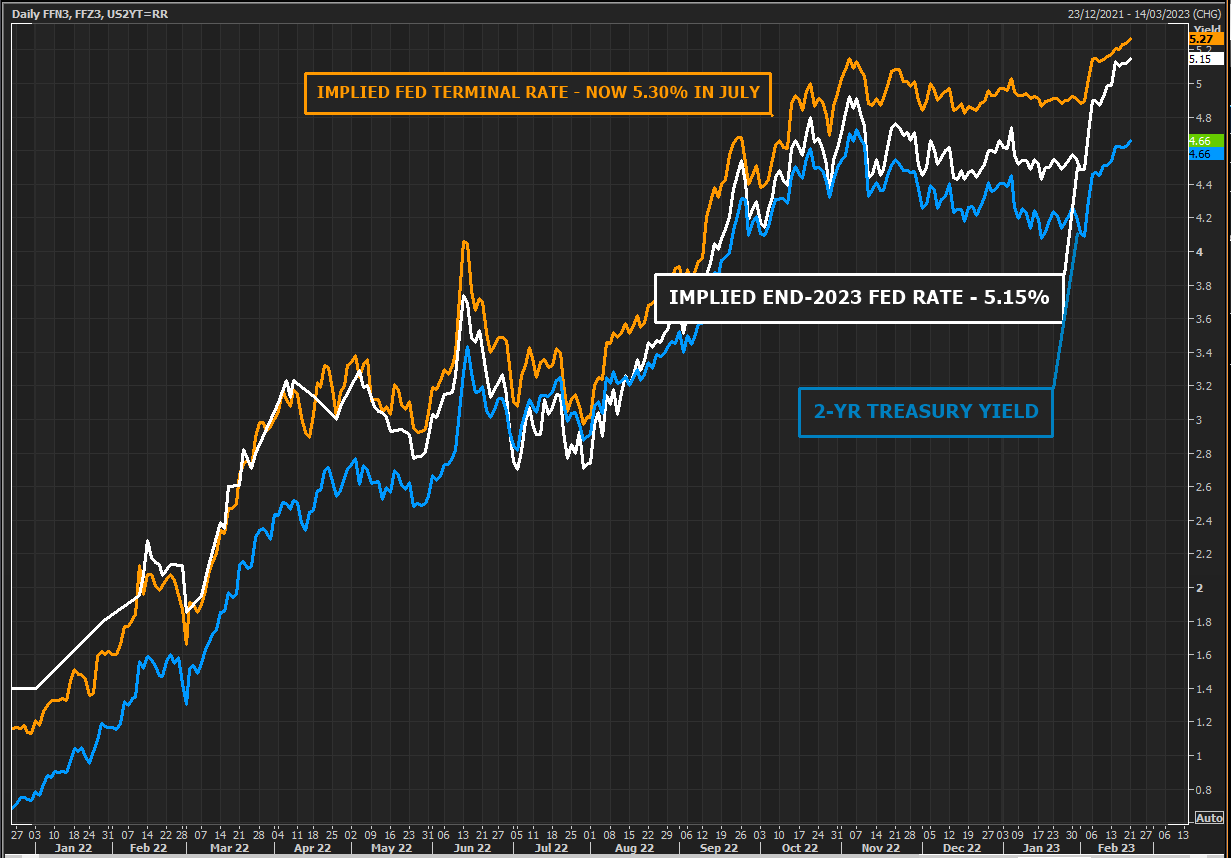

Futures markets are now pricing in a peak Fed rate at just over 5.3% in July, about 65 basis points higher than current rates. Yearend rates are priced as high as 5.11%. Two-year U.S. Treasury yields hovered just below Friday’s peaks at 4.68% ahead of Tuesday’s auction of new paper.

With inflation and rates worries to the fore, equity markets see the glass half empty – mixed to lower in Europe and Asia on Tuesday, with U.S. stock futures in the red ahead of the open.

The dollar was marginally higher, mostly against the euro and yen. The Japanese currency was dampened by less ebullient Japanese manufacturing sentiment.

Sterling was the big gainer on the surprise jump in UK services.

Aside from Tuesday’s business surveys, a reality check for U.S. retailers is due from Walmart and Home Depot’s quarterly earnings – holding last month’s red-hot retail numbers up to the light.

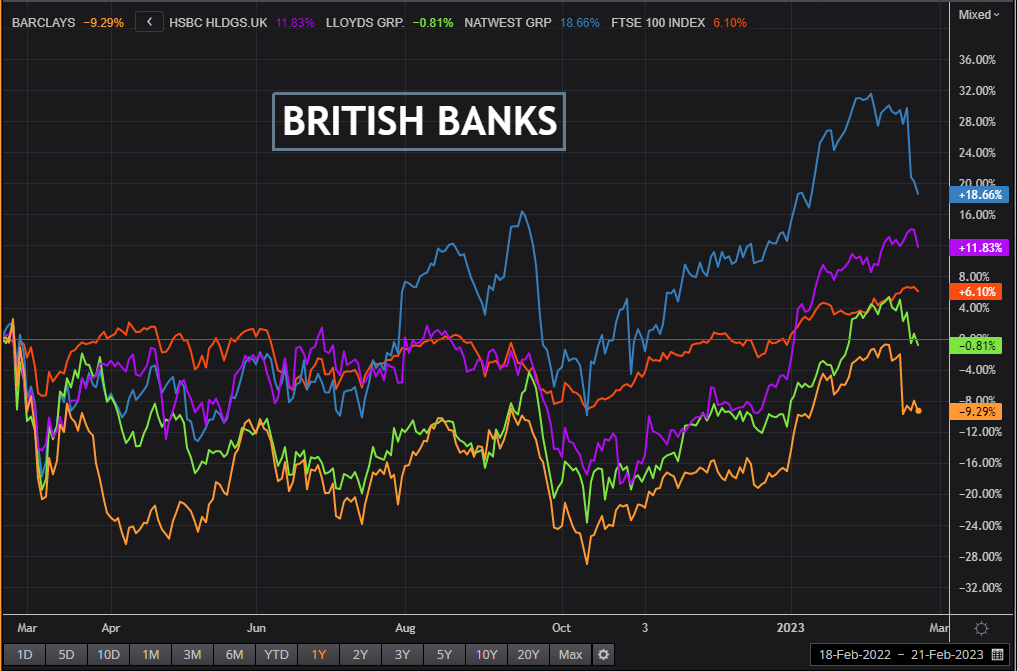

In banking, HSBC rose 1.5% – bouncing back from early losses after announcing a surge in its quarterly profit.

Even though HSBC dampened investors’ expectations of a sustained income bonanza from rising global interest rates, Europe’s biggest bank reported a 92% surge in quarterly profit and pledging more regular dividends and share buybacks.

Key developments that may provide direction to U.S. markets later on Tuesday:

* U.S. and global flash business surveys for Feb. Philadelphia Fed’s Feb non-manufacturing activity, Jan existing home sales, Canada Jan inflation and retail sales

* U.S. Treasury sells 2-year notes

* U.S. corp earnings: Walmart, Home Depot, Molson Coors, Caesars Entertainment, Medtronic.

(By Mike Dolan, editing by XXXX mike.dolan@thomsonreuters.com. Twitter: @reutersMikeD, Editing by Louise Heavens)

About the Author

Reuterscontributor

Reuters, the news and media division of Thomson Reuters, is the world’s largest international multimedia news provider reaching more than one billion people every day. Reuters provides trusted business, financial, national, and international news to professionals via Thomson Reuters desktops, the world's media organizations, and directly to consumers at Reuters.com and via Reuters TV. Learn more about Thomson Reuters products:

Advertisement