Advertisement

Advertisement

Dysfunction in ‘wildly illiquid’ bond markets unnerves investors, officials

By:

By Dhara Ranasinghe, Yoruk Bahceli and Davide Barbuscia

By Dhara Ranasinghe, Yoruk Bahceli and Davide Barbuscia

LONDON (Reuters) – Wild price swings in government bonds on a scale not seen in decades given banking sector turmoil have sparked concern about the smooth functioning of a market considered vital to the global financial system.

Trading in short-dated German bond futures was briefly interrupted due to volatility after Thursday’s European Central Bank’s rates decision and on Wednesday CME Group briefly halted trade in some U.S. interest rate futures.

Separately, two days of chaos in China’s $21 trillion bond market ended on Friday after Beijing allowed money brokers to resume providing data to third-party platforms.

Extreme intraday price swings in government bonds, used as benchmarks for the pricing of a host of other assets, is another headache for officials navigating banking sector turmoil that has drawn parallels with the 2008 global financial crisis.

Jeffrey Gundlach, CEO of DoubleLine Capital, said he considered selling Treasuries earlier in the week but the market was “wildly illiquid.”

“The strangest bond day ever was Tuesday this week where if you took your eyes off the Treasury market screen for one minute …When you looked back at the screen the price could be a point different on 10 years, 30 years (bonds),” he said.

Euro zone benchmark bond issuer Germany’s two-year bond futures have been exceptionally volatile. On March 15, when the extent of Credit Suisse’s problems started to become apparent, the front-month futures contract saw its biggest swing between intraday highs and lows on record, according to Refinitiv data.

Two-year U.S. and German bond yields fell over 50 basis points (bps) each on Wednesday, the biggest daily moves in at least 28 years, before rising sharply the next day.

“We have seen the biggest swings in decades, that is the point of comparison,” said Nordea chief analyst Jan von Gerich.

“Across markets it’s not the same volatility as it was during the global financial crisis, but in the bond markets these are big swings and that tells me everything is not okay.”

In China meanwhile, investors grappled with a different kind of chaos.

Regulators had on Wednesday barred brokers from providing data feeds, citing data security. Turnover in the interbank bond market tumbled 9% on Wednesday and another 16% on Thursday as traders had trouble accessing price information with many turning messaging groups to trade.

Liquidity

Liquidity, the ease of buying and selling an asset, has been challenging this week.

The heads of government bond trading at two European banks said bid-offer spreads, which represent transaction costs for traders, remained wider than usual on Friday.

One said he expected liquidity would remain poor for a while.

Daniel Ivascyn, chief investment officer at PIMCO, said bond market conditions this week were not as bad as during the 2020 COVID crisis, but noted that liquidity in the $22 trillion U.S. Treasury market was “challenging”, even relative to the last couple of years.

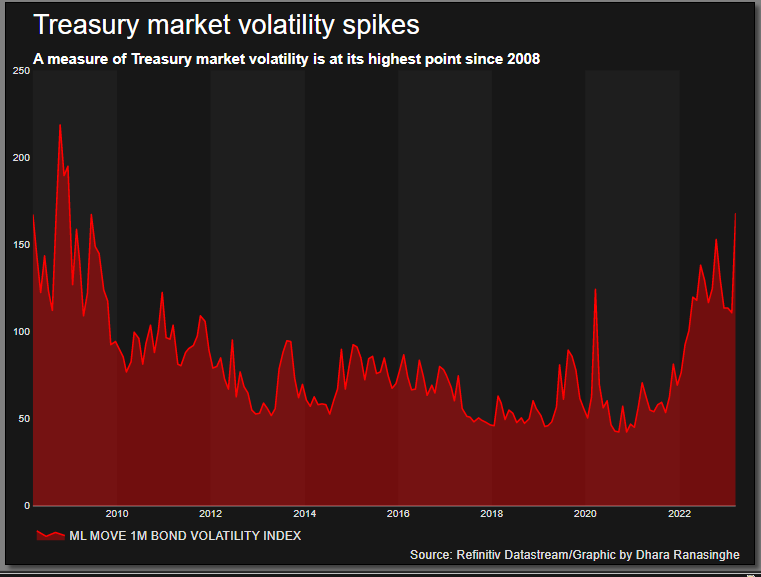

A measure of implied volatility in the Treasury market meanwhile rose this week to its highest level since 2008.

Keeping watch

The heightened volatility has caught the eye of officials who play a role in ensuring financial markets stability.

A Dutch finance ministry spokesperson told Reuters on Friday the Treasury was keeping a close eye on bond markets, adding it did not expect to make any changes to its issuance plans for the year which are already more flexible than usual.

“Of course, we will continue to closely monitor the developments in the markets. Where necessary we can adapt our plans,” the person said.

On Thursday, Germany’s debt agency said its bond market was functioning well but auctions could be affected by the volatility, while UK debt agency chief on Wednesday described global markets as “pretty stressed and volatile.”

Analysts noted that bond volatility was exceptionally high not only because of a flight to safe-haven government debt, but also due to a massive repricing of rate-hike expectations.

“Safe-haven bonds on which other assets are priced need stable valuations,” said Nordea’s Gerich. “If liquidity is deteriorating due to wild swings in safe-haven markets, that has implications for the functioning of financial markets and broader economic stability.”

(Reporting by Dhara Ranasinghe in London,Yoruk Bahceli in Amsterdam and Davide Barbuscia in New York, additional reporting by Amanda Cooper in London; Editing by Raissa Kasolowsky)

About the Author

Reuterscontributor

Reuters, the news and media division of Thomson Reuters, is the world’s largest international multimedia news provider reaching more than one billion people every day. Reuters provides trusted business, financial, national, and international news to professionals via Thomson Reuters desktops, the world's media organizations, and directly to consumers at Reuters.com and via Reuters TV. Learn more about Thomson Reuters products:

Advertisement